Irrevocable Life Insurance Trust: How an ILIT Helps Create Estate Liquidity

Updated May 5, 2026 to reflect current estate tax exposure and planning considerations.

An irrevocable life insurance trust, often called an ILIT, is a planning tool used by affluent families to keep life insurance proceeds outside of the taxable estate.

When structured properly, an ILIT can provide estate liquidity, protect assets for heirs, and help reduce the need to sell illiquid assets to pay estate taxes or other settlement costs.

For families with significant wealth, the question is not only whether they have a taxable estate. The more important question is often this:

Where will the liquidity come from when it is needed most?

Real estate, privately held businesses, investment portfolios, and other illiquid assets may create meaningful wealth. However, they may not provide immediate cash when estate taxes, administration costs, or family obligations come due. This is where life insurance owned by an ILIT can play an important role.

Irrevocable Life Insurance Trust (ILIT)

The purpose of an irrevocable life insurance trust or ILIT is to prevent life insurance death benefits from being subject to estate taxes.

An irrevocable life insurance trust involves three parties:

- The grantor or the person funding the trust.

- Trustee or person managing the trust according to the trust language.

- Beneficiary or person who will have access to or receive the trust property

Because an ILIT is irrevocable, any transfer of property to the trust cannot be transferred back without the consent of the trustee and beneficiaries.

Most irrevocable life insurance trusts will only own a life insurance policy. The grantor of the ILIT will make gifts equal to the life insurance policy premiums. In order to accomplish this, the grantor will use annual gifts or a portion of their lifetime gift tax exemption.

- The grantor makes a gift payable to the Irrevocable Life Insurance Trust (ILIT).

- The trustee deposits the check into the ILIT’s checking account. The trustee then uses the funds to purchase a permanent life insurance policy for the insured(s).

- If the policy insures a single individual the death benefit is payable to the irrevocable life insurance trust (ILIT) upon their passing. When using a survivorship life insurance policy , meaning one policy insures two lives (couples), the death benefit is payable to the Irrevocable Life Insurance Trust after the second insured’s passing.

- The trustee distributes life insurance proceeds according to the terms of the ILIT to the ILIT beneficiaries.

An ILIT Can…

- Provide lifetime benefits to a surviving spouse and/or other loved ones.

- Help meet the liquidity needs of their estate.

- Minimize income, estate, and gift taxes.

Benefits for You…

- Your legacy is preserved and the size of your taxable estate is reduced.

- You gain more control over how your loved ones receive your wealth.

- You can equalize inheritance among children and/or other loved ones.

Benefits for Your Loved Ones…

- With less lost to taxes, they’re able to enjoy more of their inherited wealth.

- They’ll have increased liquidity at at time when it may be needed most.

- They may benefit from creditor protection.

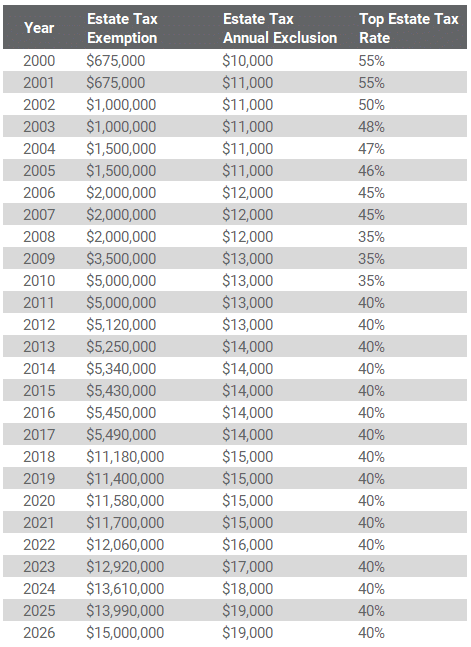

2026 Estate Tax Exemption, Annual Gift Exclusion, and Tax Rates

In 2026, the federal estate and gift tax exemption is $15 million per individual, or $30 million for a married couple. The annual gift tax exclusion remains $19,000 per beneficiary. This means an individual can give up to $19,000 per recipient in 2026 without using any lifetime exemption. Married couples may be able to combine their exclusions and gift up to $38,000 per beneficiary.

For families with estates above the exemption amount, the top federal estate tax rate remains 40%. Even with the higher exemption, many affluent families may still face estate tax exposure due to business interests, real estate, concentrated investments, or continued asset growth.

Lifetime Exemptions, Annual Exclusions, and Tax Rates 2000 – 2026

Why ILIT Planning Still Matters After the 2026 Tax Law Change

The estate tax exemption did not drop in 2026 as previously expected. However, that does not mean ILIT planning is no longer relevant.

For many families, the core issue is not only the size of the exemption. It is liquidity.

An ILIT can help provide cash at death without requiring heirs to sell a family business, real estate, investment assets, or other illiquid holdings at the wrong time.

How To Properly Structure Life Insurance With An Irrevocable Life Insurance Trust

Life insurance provides liquidity to help pay estate taxes.

Not only does life insurance provide the cash to pay the estate tax, but it can also keep the estate from having to sell assets to pay the tax.

This makes life insurance one of the most highly-efficient and simple ways for families to transfer their estates to heirs.

When properly structured, proceeds from a life insurance policy are income and estate tax-free.

The key is structuring the ownership and beneficiary of the life insurance policy properly.

We want to make sure the death benefit is not included in the estate and is not subject to estate taxes. Especially when it is easily avoidable.

When considering life insurance for estate planning the first steps are to determine:

- How much coverage do you need?

- Are the needs of the estate for individual or survivorship life insurance?

- What carriers and products offer the best pricing and underwriting?

Individual life insurance coverage pays a death benefit when the individual dies. Survivorship life insurance coverage pays the death benefit after the second insured dies. Other names for survivorship life insurance include joint-survivor or second-to-die life insurance. It is usually less expensive than individual life insurance coverage.

Once these steps are complete and the decision is to move forward, the next step is to complete underwriting and draft the trust.

Irrevocable Life Insurance Trust (ILIT) Benefits

Irrevocable life insurance trusts offer a number of benefits. These include:

- Providing immediate liquidity to help minimize estate taxes or expenses of an estate.

- Maximize control over the distribution of death benefit proceeds to beneficiaries.

- Proceeds received by an ILIT are generally protected from creditors of the irrevocable life insurance trusts beneficiaries until they receive actual trust proceeds.

- Equalize inheritance when the grantor would like to pass down a single asset (e.g. business or real estate) to one child while providing equal value for other children.

- Avoid gift tax issues.

When Does an Irrevocable Life Insurance Trust Make Sense?

An ILIT is not necessary for every family. However, it may be worth considering in situations where:

- The estate is projected to exceed the current federal exemption

- A significant portion of wealth is tied up in illiquid assets such as real estate or a closely held business

- There is a desire to create liquidity without disrupting long-term investments

- The goal is to provide equalization among heirs, particularly when certain assets are not easily divisible

- There is a need for creditor protection or structured distributions for beneficiaries

Even for families below the exemption threshold today, continued asset growth, concentrated holdings, and future legislative uncertainty may still justify planning.

Life Insurance Underwriting

When a life insurance company underwrites an individual for coverage the insurance company will review medical history and records, financial information, and other items necessary to determine your underwriting class and to make sure the requested death benefit is suitable.

The insured will complete some form of a medical exam by a third-party examiner paid for by the insurance company prior to the policy issue. Life insurance exam requirements vary based on the face amount of the policy and the carrier. At a minimum, this will include height, weight, blood, and urine analysis.

The insurance carrier will make an underwriting or health class offer once they receive and review all the information. This is what will determine the pricing of the life insurance policy.

Informal Underwriting

If you or your spouse have any medical history or if there are any questions about what underwriting health class you might be, we recommend applying for coverage on an informal basis.

This allows us to obtain your medical records and submit them to multiple insurance companies for “informal offers.” After reviewing the medical records, each insurance company will make tentative underwriting or health class offers subject to a list of requirements to secure the actual policy.

In this example, medical records were submitted to eight different life insurance companies. Of the eight companies, only three of them were able to make offers.

Upon receipt of the informal offers, we evaluate the impact of these offers on the pricing of each policy. This allows us to recommend the life insurance policy most suitable for the given fact pattern.

Formal Underwriting

Formal underwriting begins when a carrier receives the life insurance application. Each life insurance company has its own application.

When applying for life insurance for estate planning it is critical to set up the ownership and beneficiary properly. Failure to do so could result in the death benefit being subject to estate taxes.

By naming your irrevocable life insurance trust (ILIT) as the owner and beneficiary of the policy death benefit proceeds should avoid income and estate taxes.

To accomplish this, the trustee of the ILIT will sign as the owner of the policy.

In addition, most life insurance companies will require the completion of a “Trust Certification” form as a part of the application.

Since formal underwriting can take a few weeks, many people choose to have their ILIT drafted to coincide with underwriting.

There are situations where a formal application is submitted before an ILIT has been drafted or executed. When taking this approach, it is important to list the owner on the application as “to be determined” or “pending”.

This allows the life insurance company to continue underwriting the policy, while the creation of the ILIT is occurring. Upon execution of the ILIT, the insurance company will require additional paperwork to reflect the ILIT as the owner and beneficiary of the policy.

The date of life insurance application should ALWAYS be after the execution date of the irrevocable life insurance trust (ILIT).

Once the requirements are complete, the insurance company will issue the policy.

Crummey Letters

When using annual gifts to fund an ILIT the trustee should send out “Crummey letters” to trust beneficiaries. This should take place in any year a gift is made to the irrevocable life insurance trust.

“Crummey letter” serves to inform the trust beneficiaries of their ability to withdraw the gifted amount during a specified window. Usually 30-days.

The IRS will only consider it a tax-free gift if the person has the ability to take it in the short term. By doing this, the trustee can make sure the life insurance death benefit remains outside of the estate.

ILIT vs Personally Owned Life Insurance

Life insurance can provide liquidity, whether it is owned personally or by a trust. However, ownership structure can have a significant impact on estate inclusion.

When a policy is owned personally, the death benefit is generally included in the insured’s taxable estate.

When owned by an ILIT and structured properly, the death benefit is typically excluded from the estate, allowing proceeds to pass outside of estate taxation.

This distinction can meaningfully impact the net amount received by heirs, particularly for larger policies.

What If I Already Have a Life Insurance Policy, But It Isn’t Owned by an Irrevocable Trust?

If you already have a life insurance policy, you can transfer it to an irrevocable life insurance trust.

To do this you need to submit the proper ownership and beneficiary change forms to the life insurance company. You can get this paperwork by contacting the carrier directly or your life insurance advisor.

Prior to doing so, it is important to determine if there will be any transfer for value issues. Completing a valuation on the policy prior to transferring it to the irrevocable trust will avoid any valuation issues in the future.

Before making any changes make sure you have an irrevocable life insurance trust set up and executed. In addition, the trustee will need to sign as the new owner of the policy.

If you pass away within three years of changing the ownership the death benefit will likely be subject to estate taxes.

Also, we encourage you to speak with your agent, accountant, or tax attorney to make sure you do not incur any income taxes because of the transfer.

Common ILIT Planning Mistakes to Avoid

While ILITs can be highly effective, improper structuring can reduce their benefits. Some common issues include:

- Failing to properly fund the trust or coordinate premium payments

- Not adhering to Crummey notice requirements for annual gifts

- Transferring an existing policy without considering the three-year inclusion rule

- Selecting trustees who are not aligned with the long-term intent of the trust

- Failing to periodically review the policy performance within the ILIT

Ongoing coordination between the client, CPA, attorney, and advisor is critical.

Final Thoughts on Irrevocable Life Insurance Trusts

The effectiveness of an ILIT depends on how it is structured, funded, and coordinated with the rest of your estate plan.

If you would like to better understand how an ILIT could impact your estate, we can walk through a customized analysis based on your current assets, projected growth, and liquidity needs.

Schedule a call to explore how this strategy may fit within your broader planning framework.

Last updated May 5, 2024

DISCLOSURE

TAX ADVICE

Any tax advice contained in this communication is not intended or written to be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing, or recommending to another party any transaction or matter addressed herein.

These materials are not intended to be opinions or advice on legal, tax, accounting, or investment matters. Private counsel should be consulted prior to the application of this general information to specific situations.

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Jason Mericle

Founder

Jason Mericle created Mericle & Company to provide families, business owners, and high net worth families access to unbiased life insurance information.

With more than two decades of experience, he has been involved with helping clients with everything from the placement of term life insurance to highly sophisticated and complex income and estate planning strategies utilizing life insurance.

Stay In The Know

Get exclusive tips and practical information to help you create, grow, sustain, and protect your wealth.

Ask Us Anything

We Are Here To Answer Your Questions

Start A Conversation

Schedule a complimentary 30 minute Zoom meeting to learn more about your options.