Premium Financing Life Insurance Case Study: How to Create Estate Liquidity Without Selling Assets

Updated April 2026 to reflect current estate tax exposure and planning considerations.

Premium financing life insurance has become an increasingly important strategy for affluent families facing estate tax exposure. While many estate plans appear complete on paper, one critical question often remains unanswered:

Where will the liquidity come from to settle estate obligations without disrupting the assets that define the family’s wealth?

In this premium financing case study, we walk through how a high-net-worth family used a structured financing strategy to create more than $20 million in estate liquidity – without liquidating core assets or compromising long-term growth.

This premium financing strategy is often used by high-net-worth families to solve estate liquidity challenges in a capital-efficient way.

Understanding how premium financing life insurance works is critical when evaluating whether this strategy fits within a broader estate plan.

What Is Premium Financing Life Insurance and How Does It Work?

Premium financing is a strategy that allows individuals or trusts to borrow funds from a third-party lender to pay life insurance premiums. Rather than using personal capital, the client leverages borrowed funds – typically secured by the policy’s cash value and additional collateral.

This approach is commonly used in estate liquidity planning for high-net-worth individuals who want to preserve their balance sheet while still creating a meaningful death benefit. When structured properly, premium financing can provide a capital-efficient way to address estate tax exposure while maintaining flexibility.

Client Profile

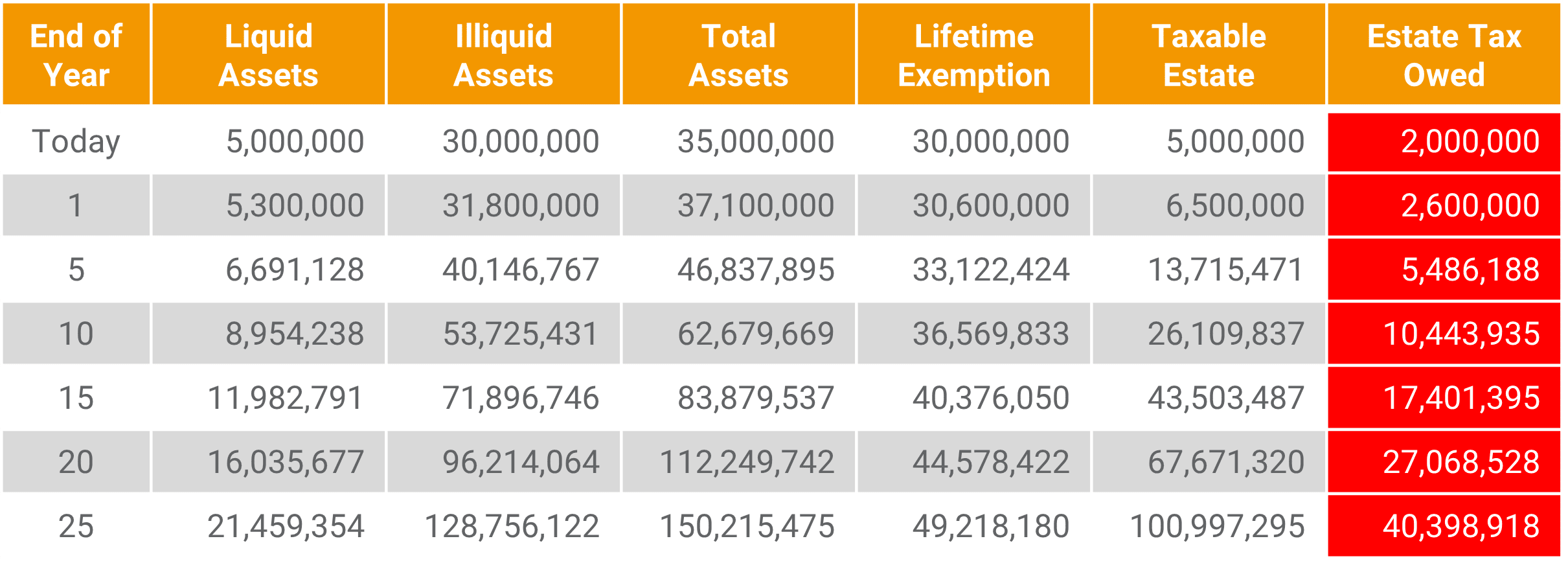

The client was a married couple in their early 60s with an estimated net worth of approximately $35 million. Like many families in this position, the majority of their wealth was concentrated in illiquid or tax-sensitive assets, including a closely held business, commercial real estate holdings, and a diversified investment portfolio with significant embedded gains.

While their balance sheet was strong, their liquidity position was limited relative to their projected estate tax exposure. Based on current projections, their estate faced a potential tax liability exceeding $20 million, depending on future exemption levels and asset growth.

The Problem: A Significant Liquidity Gap

The core issue was not whether estate taxes would be owed – it was how those taxes would be paid.

Without a structured plan, the family faced the possibility of being forced to sell business interests or real estate holdings at an inopportune time. Liquidating appreciated assets would also introduce additional tax consequences, further reducing the value passed to heirs.

This is a common challenge in estate liquidity planning, where balance sheet strength does not necessarily translate into usable cash at the time it is needed most.

Why Traditional Planning Approaches Fell Short

Several traditional strategies were evaluated before implementing premium financing.

Self-funding a life insurance policy would have required a significant out-of-pocket commitment, reducing the assets available for investment and long-term growth. While effective in some cases, this approach did not align with the client’s desire to preserve capital.

Gifting strategies, including funding an irrevocable life insurance trust, were also considered. However, given the size of the premiums required and the client’s interest in preserving flexibility, this approach was not optimal as a standalone solution.

Waiting was another option – but one that increased risk. As asset values grow and lifetime gift tax exemption levels remain uncertain, the potential estate tax liability – and corresponding liquidity gap – can expand over time.

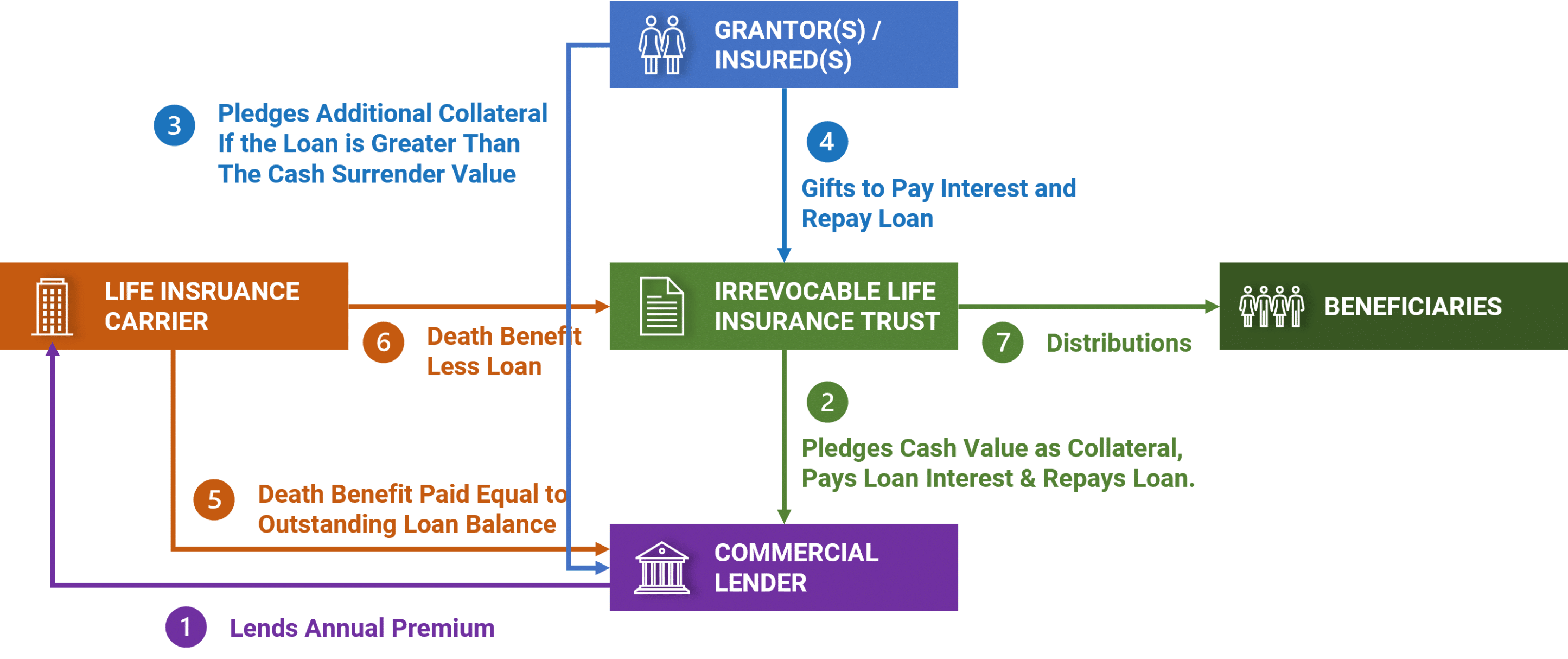

How Premium Financing Life Insurance Works in Practice

To address these challenges, the client implemented a premium financing life insurance strategy designed to create significant leverage while minimizing immediate capital outlay.

A survivorship life insurance policy was established and owned by a trust for estate planning purposes. Instead of funding premiums directly, the trust entered into a financing arrangement with a third-party lender.

The loan was structured with flexibility in mind, including defined collateral requirements and multiple exit strategies. These included the potential to repay the loan through asset repositioning, refinancing, or policy performance over time.

This structure allowed the clients to maintain their existing investment strategy while still creating a substantial pool of future liquidity.

Premium Financing vs. Self-Funding Life Insurance

When evaluating premium financing life insurance, the decision often comes down to capital efficiency and liquidity preservation.

Self-funding requires a direct allocation of capital toward premiums, which may reduce long-term investment growth. Premium financing, by contrast, allows clients to preserve their balance sheet while leveraging borrowed funds to create a death benefit.

However, this approach introduces additional considerations, including interest rate exposure and collateral requirements. The appropriate strategy depends on the client’s financial profile, risk tolerance, and long-term objectives.

The Outcome: Creating Estate Liquidity – Without Disruption

Through this premium financing strategy, the client was able to secure more than $20 million in life insurance death benefit, specifically designed to address estate tax obligations.

Importantly, this was accomplished without requiring the liquidation of business interests, real estate, or other core assets. Instead of redirecting significant capital into premium payments, the clients maintained their investment strategy while still solving their liquidity challenge.

From an efficiency standpoint, the strategy created meaningful leverage – transforming a relatively modest out-of-pocket commitment into a substantial source of tax-advantaged liquidity.

Should You Consider Premium Financing Life Insurance?

Premium financing life insurance is not appropriate for every situation. It is typically considered by high-net-worth individuals with significant estate tax exposure and a desire to preserve liquidity.

The decision often depends on factors such as asset composition, risk tolerance, and the ability to manage collateral requirements over time. For those with concentrated or illiquid holdings, this strategy can offer a way to create estate liquidity without disrupting long-term investment plans.

Key Considerations

While premium financing life insurance can be a powerful planning tool, it requires careful structuring and ongoing management.

Interest rate risk is a key consideration, particularly in changing rate environments. Collateral requirements must also be evaluated, as additional assets may be required to support the loan over time.

Understanding the risks of premium financing life insurance – including interest rate exposure and collateral requirements – is essential before implementing the strategy.

Equally important is the exit strategy. A well-designed plan outlines how the financing arrangement will be resolved, ensuring alignment with long-term estate and financial objectives.

As with any advanced planning strategy, coordination with legal, tax, and advisory professionals is essential.

When Premium Financing May Be Appropriate

Premium financing is typically most effective for individuals or families with a net worth in excess of $15–$20 million, particularly when a large portion of assets are illiquid or tax-sensitive.

It is often considered in situations where there is clear estate tax exposure and a desire to preserve capital rather than allocate it to insurance premiums. In these cases, premium financing can provide a way to create liquidity efficiently while maintaining flexibility.

Final Thoughts

Premium financing life insurance is not simply a product-driven strategy – it is a tool used to solve a specific problem: creating liquidity where it does not naturally exist.

When integrated into a broader estate plan, it can help ensure that assets are transferred intentionally, without disruption or forced decisions.

Explore Your Options

If you are evaluating how to address estate tax exposure and create liquidity without disrupting your broader financial strategy, we can help you model what may be possible.

The goal is not to force a solution – but to provide clarity around your options.

Schedule a confidential consultation to evaluate what may be possible.

Jason Mericle

Founder

Jason Mericle created Mericle & Company to provide families, business owners, and high net worth families access to unbiased life insurance information.

With more than two decades of experience, he has been involved with helping clients with everything from the placement of term life insurance to highly sophisticated and complex income and estate planning strategies utilizing life insurance.

Stay In The Know

Get exclusive tips and practical information to help you create, grow, sustain, and protect your wealth.

Ask Us Anything

We Are Here To Answer Your Questions

Start A Conversation

Schedule a complimentary 30 minute Zoom meeting to learn more about your options.