How Affluent Families Engineer Estate Liquidity to Avoid Forced Asset Sales

Estate liquidity planning is often assumed to be complete once trusts are drafted and life insurance is in place. On paper, everything looks organized.

But one critical question is rarely modeled:

If a large estate tax bill arrives, where does the cash actually come from?

Estate liquidity planning refers to the process of ensuring an estate has sufficient liquid assets available to pay estate taxes and settlement costs without forcing the sale of illiquid assets such as real estate or closely held businesses.

For affluent families with concentrated real estate, closely held businesses, or highly appreciated assets, net worth does not equal liquidity. Estate taxes are typically due within nine months, regardless of market conditions. Without proper estate liquidity planning, heirs may be forced to sell assets under pressure rather than by choice.

In fact, many families only discover the problem after reviewing the dynamics discussed in our guide on Estate Liquidity: Planning Before the Event, Not After It.

Owning a policy is not the same as engineering liquidity. Effective estate liquidity planning requires projecting estate tax exposure, identifying the liquidity gap, and designing a funding strategy that can withstand changing tax laws — including the potential sunset of today’s elevated lifetime exemption.

The difference between guessing and engineering is clarity. And clarity protects a family’s legacy.

Liquidity Is a Math Problem Before It’s an Insurance Problem

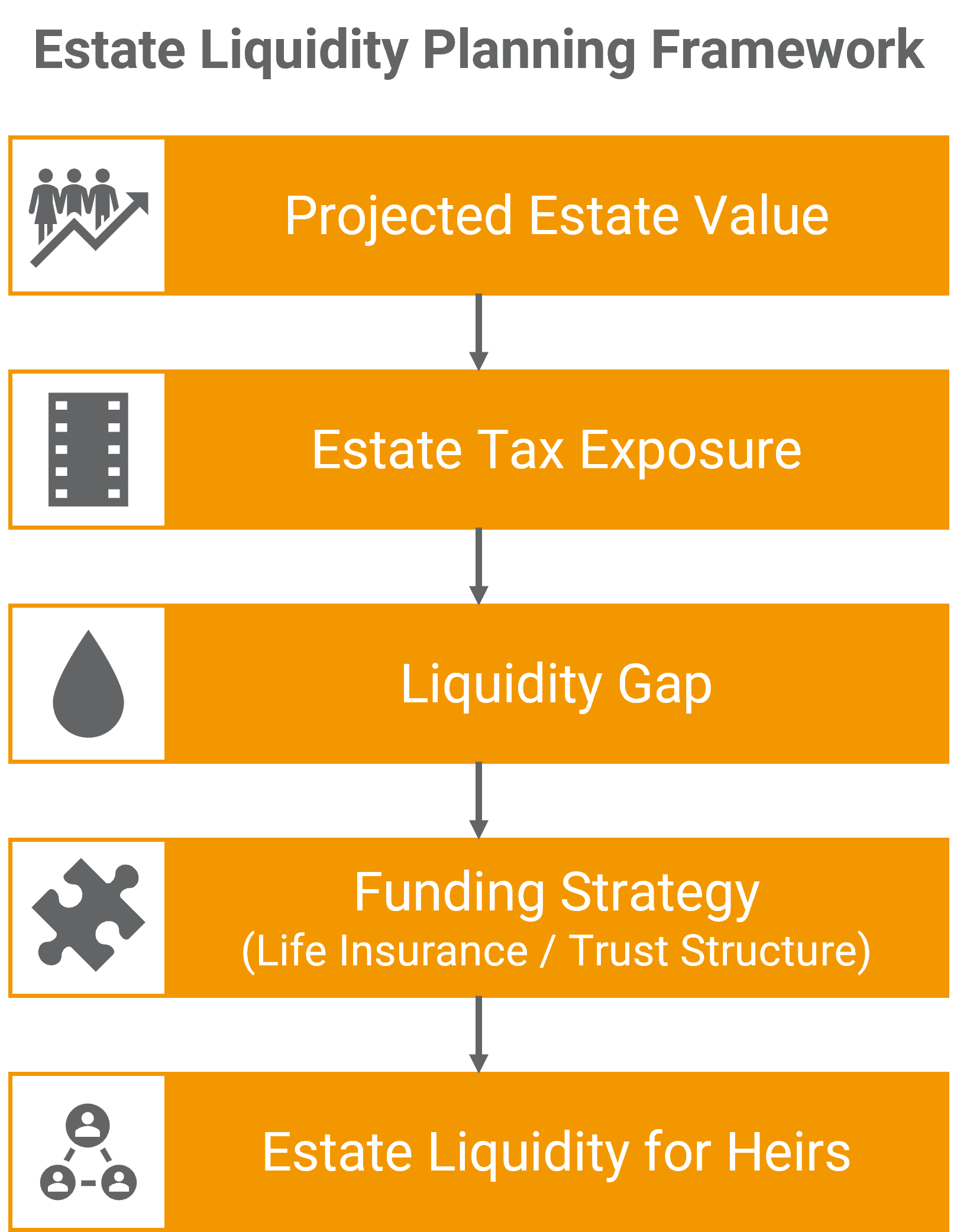

When families think about estate liquidity, the conversation often begins with life insurance. In reality, insurance should not be the starting point. The starting point is clarity.

Before any policy is designed, families need to understand what their estate may look like years from now. That means projecting the value of real estate, business interests, investment portfolios, and other appreciating assets – and then estimating the estate tax exposure under current law, including the possibility that today’s elevated lifetime gift tax exemption may not last.

Only after running these projections can the true liquidity gap be identified.

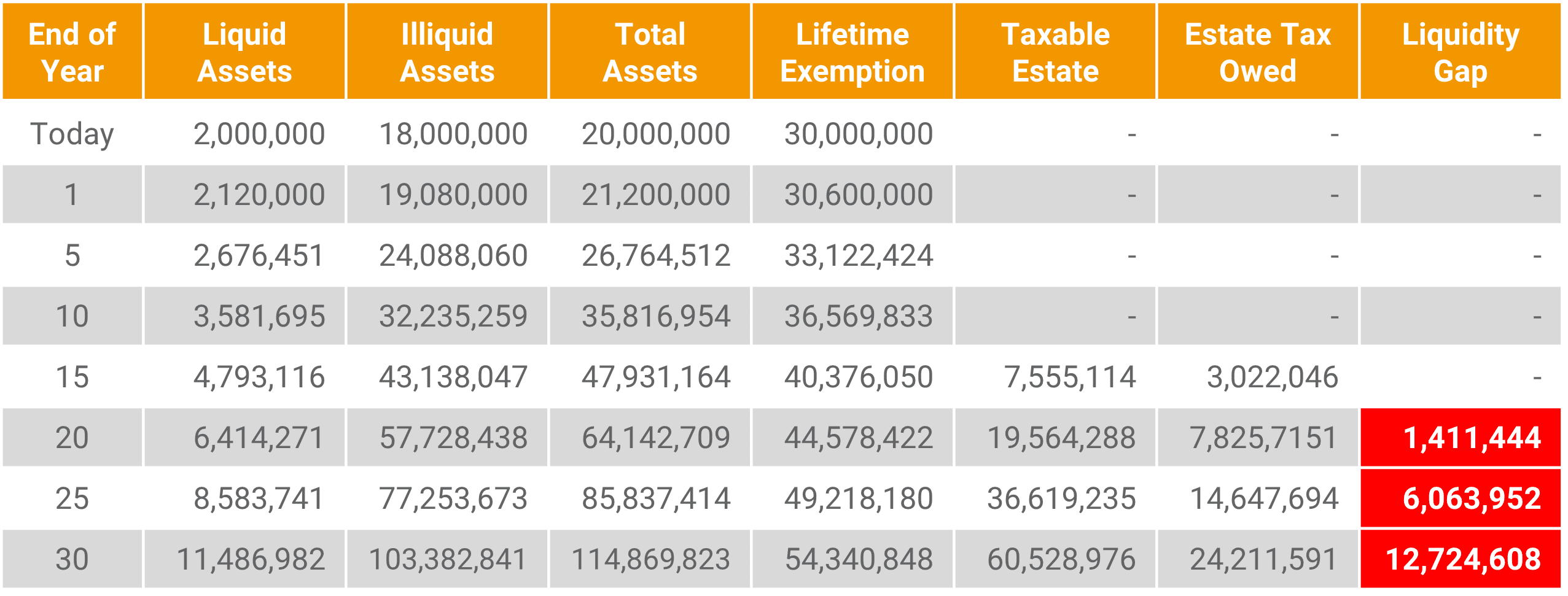

A liquidity gap represents the difference between the estate tax that may be due and the liquid assets that would realistically be available to pay it, without forcing the sale of a business, a real estate portfolio, or a concentrated investment position. Many affluent families are surprised to discover that while their net worth is substantial, their accessible liquidity may be limited.

Projected Estate Value vs Liquidity Gap

As estates grow over time, the gap between total asset value and available liquidity can widen significantly. Without planning, families may be forced to sell assets to satisfy estate tax obligations.

Timing complicates the equation further. Federal estate taxes are generally due within nine months. Markets do not pause. Buyers may not appear immediately. Financing options may not be ideal. Estate liquidity planning must account for when liquidity will be needed, not just how much.

With the liquidity gap clearly defined, the next step is designing a structure capable of reliably closing the gap.

The Design Decisions That Determine Whether Liquidity Actually Works

Once projected estate tax exposure and liquidity needs are understood, thoughtful design becomes critical. Estate liquidity planning involves several coordinated decisions that must work together over time.

One of the first considerations is ownership. In many cases, families use an irrevocable life insurance trust so that the policy’s death benefit is excluded from the taxable estate. In other circumstances, business ownership or alternative structures may be appropriate depending on the broader planning strategy. The ownership decision influences tax treatment, control, and long-term flexibility.

The next consideration is funding. Premiums may be funded through annual gifting, through larger upfront contributions, or in some cases through structured financing strategies. Each approach carries different implications for cash flow, gift tax usage, and long-term sustainability.

Policy design is another important factor. Different policy structures offer varying combinations of guarantees, flexibility, and long-term efficiency.

Finally, estate liquidity planning requires ongoing oversight. Policies should be periodically reviewed, assumptions should be tested, and estate projections should be updated as circumstances evolve.

When these decisions are made deliberately, estate liquidity becomes engineered rather than assumed.

Where Estate Liquidity Plans Quietly Break Down

Most estate liquidity strategies do not fail suddenly. They drift.

The policy is issued, premiums are paid, and statements are filed away. Over time, however, estates grow, markets change, and assumptions embedded in the original design begin to shift.

One common issue is underfunding. Policies designed under certain crediting assumptions may require more disciplined funding than originally anticipated. When contributions fall short of projections, the long-term durability of the coverage can weaken.

Another issue arises when estate projections become outdated. Appreciating real estate, business growth, or concentrated investment positions can expand the estate faster than originally modeled. When that happens, the liquidity gap may widen beyond the amount originally insured.

Administrative oversight can also become an issue. If an irrevocable trust owns the policy, trustees must follow proper procedures, including required Crummey notices and documentation. Over time, these responsibilities may be overlooked if the strategy is not periodically reviewed.

Without ongoing oversight, families may assume their liquidity plan is functioning exactly as intended. When in reality, the strategy has not been revisited, and a life insurance policy review has not been completed for a couple of years.

Estate liquidity planning should not be viewed as a one-time transaction. It is a long-term strategy that benefits from periodic modeling and review.

Engineering vs. Buying: Why the Distinction Matters

For many families, estate liquidity planning begins with a product conversation. A policy is recommended, coverage is placed, and the issue is considered solved.

But effective estate liquidity planning rarely works that way.

Engineering estate liquidity begins with understanding the estate itself — its projected growth, its asset composition, and the potential tax exposure that may arise in the future. From there, the liquidity gap can be measured, ownership structures coordinated, and funding strategies designed to remain intact over time.

In that context, life insurance becomes an implementation tool rather than the starting point.

When structured thoughtfully, insurance can provide predictable liquidity exactly when it is needed, allowing families to preserve businesses, retain long-held real estate, and maintain control over how assets transition to the next generation.

Estate liquidity planning is ultimately about protecting options. It allows families to determine how assets are transferred, rather than allowing tax deadlines to dictate those outcomes.

How Do Affluent Families Pay Estate Taxes Without Selling Assets?

One of the most common concerns families have is how estate taxes will actually be paid when they come due. Because federal estate taxes are generally due within nine months, families may not have the flexibility to wait for favorable market conditions or a strategic asset sale.

Without proper estate liquidity planning, heirs may be forced to sell real estate, business interests, or investment assets simply to generate the cash required to satisfy the tax obligation.

Affluent families often address this challenge by planning liquidity in advance. Strategies may include maintaining liquid reserves, structuring trusts to hold liquid assets outside the taxable estate, or using properly designed life insurance to create liquidity precisely when it is needed.

When liquidity is planned intentionally, estate taxes can be paid without forcing the next generation to make rushed decisions about long-held, family assets.

Model Your Estate Liquidity Strategy

If your estate includes real estate, business interests, or other appreciating assets, understanding your future liquidity needs is an important part of protecting your long-term plan.

A structured review can help clarify potential estate tax exposure and determine whether your current estate liquidity planning strategy is aligned with your objectives.

Request a Private Liquidity Review

Conversations are confidential and typically begin with a high-level discussion of your estate structure and liquidity objectives.

Jason Mericle

Founder

Jason Mericle created Mericle & Company to provide families, business owners, and high net worth families access to unbiased life insurance information.

With more than two decades of experience, he has been involved with helping clients with everything from the placement of term life insurance to highly sophisticated and complex income and estate planning strategies utilizing life insurance.

Stay In The Know

Get exclusive tips and practical information to help you create, grow, sustain, and protect your wealth.

Ask Us Anything

We Are Here To Answer Your Questions

Start A Conversation

Schedule a complimentary 30 minute Zoom meeting to learn more about your options.