Lifetime Gift Tax Exemption in 2026: What High-Net-Worth Families Need to Know

The federal lifetime gift and estate tax exemption has been one of the most discussed planning topics of the past several years. For affluent families, it has shaped decisions around large gifts, irrevocable trusts, and liquidity strategy.

Much of the urgency stemmed from the scheduled sunset of the Tax Cuts and Jobs Act (TCJA), which was expected to reduce the exemption after 2025. That concern drove meaningful planning activity across 2024 and 2025.

As of January 1, 2026, the law provides greater clarity.

Understanding where the lifetime gift tax exemption stands today — and how it fits into long-term estate design — remains essential for families with significant and growing wealth.

What Is the Lifetime Gift Tax Exemption?

The lifetime gift tax exemption is the total amount an individual may transfer during life or at death without triggering federal estate or gift tax.

The federal estate and gift tax systems are unified. Taxable lifetime gifts reduce the exemption available at death. Transfers above the available exemption are generally taxed at a top federal rate of 40%.

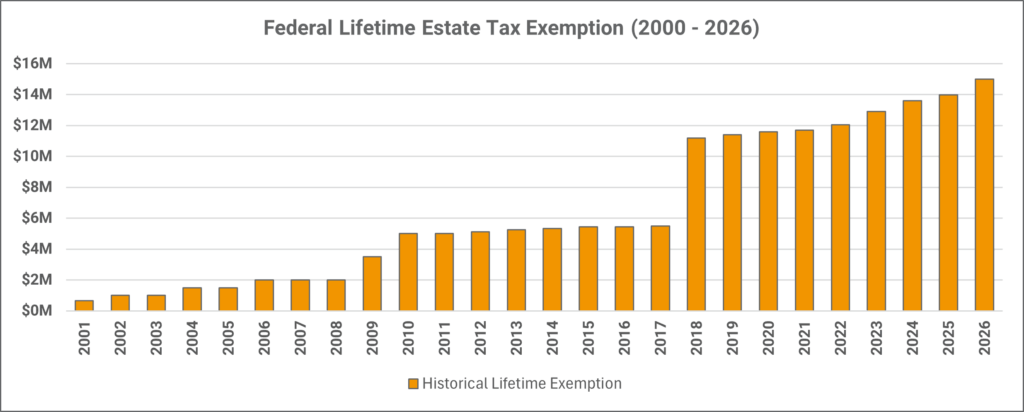

Federal lifetime estate and gift tax exemption amounts have changed significantly over time. Legislative adjustments have historically altered planning thresholds.

In addition to the lifetime exemption, individuals may make annual exclusion gifts — $19,000 per recipient in 2026 — without using any portion of their lifetime exemption. Married couples who elect gift splitting may effectively double that amount.

For 2026, the federal lifetime estate and gift tax exemption is $15 million per individual, indexed annually for inflation. With proper coordination and portability planning, a married couple may effectively shield approximately $30 million from federal estate tax.

While the exemption amount is historically high, planning should not focus solely on the number.

<INSERT LIFETIME EXEMPTION GRAPHIC FROM ILITMAP>

Where the Lifetime Exemption Stands After 2025

Under prior law, the TCJA was scheduled to sunset at the end of 2025. That sunset would have reduced the exemption significantly beginning in 2026.

Because of that statutory schedule, many families accelerated planning — particularly large lifetime gifts to irrevocable trusts — before the anticipated reduction.

Subsequent legislative changes addressed the sunset concern and established a higher indexed exemption beginning in 2026. The immediate “use it before it drops” pressure has eased.

However, the broader planning framework remains relevant.

The exemption amount is one variable in estate design. Asset growth, liquidity risk, and structural flexibility often matter more over time.

The No Clawback Rule: Why Prior Planning Remains Protected

A key technical concern during the sunset discussion was whether gifts made under higher exemption levels could later be “clawed back” if the exemption were reduced.

Treasury regulations clarified that there is no clawback of lifetime gifts made while exemption levels were higher. In practical terms, families who used elevated exemption amounts prior to 2026 retain the benefit of those transfers.

This regulatory clarity reinforced a core estate planning principle: acting under known rules can provide durable advantages, even if future legislation changes.

For families who implemented irrevocable trust strategies before 2026, those decisions remain structurally sound.

Why the Lifetime Gift Tax Exemption Still Matters in 2026

Although the exemption remains elevated, three strategic realities continue to drive planning discussions among affluent families.

Exemption Levels Are Legislative, Not Permanent

Estate tax exemptions are political. They have fluctuated significantly over the past two decades. Future legislative changes — whether higher or lower — remain possible.

Planning that relies entirely on today’s exemption level assumes legislative stability. Sophisticated families typically prefer flexibility over assumption.

Asset Growth Can Create Exposure Over Time

For families with concentrated business interests, private equity holdings, real estate portfolios, or rapidly appreciating assets, growth often outpaces exemption increases.

A $20 million estate today can become substantially larger over the next decade. Removing future appreciation from the taxable estate through lifetime gifting can produce meaningful long-term tax efficiency.

In many cases, the strategic objective is not simply to use exemption — it is to transfer growth.

Estate Liquidity Often Drives Planning Decisions

Even when projected estate tax exposure appears manageable, liquidity risk can create structural vulnerability.

Federal estate taxes are generally due nine months after death. Estates heavily weighted toward illiquid assets may be forced to sell business interests or real estate under unfavorable conditions.

Lifetime exemption planning frequently intersects with liquidity strategy. Properly structured irrevocable trusts — often funded with life insurance — can create liquidity without requiring asset liquidation.

In these cases, the exemption is a mechanism. The objective is stability.

For many families, lifetime gifting intersects directly with broader estate liquidity planning, particularly when significant assets are illiquid or closely held.

How Affluent Families Structure Lifetime Exemption Planning

The lifetime gift tax exemption is rarely implemented through simple outright transfers. Instead, it is typically coordinated through carefully designed structures that balance tax efficiency, asset protection, and control.

Common strategies include irrevocable trusts for descendants, Spousal Lifetime Access Trusts (SLATs), generation-skipping planning, and Irrevocable Life Insurance Trusts (ILITs).

When life insurance is incorporated, design discipline becomes critical. Ownership structure, funding methodology, policy selection, premium strategy, and long-term monitoring all influence outcomes.

At Mericle & Company, our focus is not limited to policy placement. We evaluate how life insurance integrates with the broader estate plan, projected liquidity needs, and the family’s long-term asset profile. The exemption creates opportunity. Structure determines durability.

Planning Beyond the Exemption Amount

Sophisticated estate planning in 2026 is less about reacting to exemption thresholds and more about designing resilient structures.

The key questions tend to be forward-looking:

- How will asset growth affect estate exposure over the next 10 to 20 years?

- Where will liquidity come from when obligations arise?

- How can trusts be structured to maintain flexibility while preserving tax efficiency?

- How should life insurance be designed to support — not complicate — the plan?

Families with $20 million or more in net worth, particularly those with illiquid or concentrated holdings, often benefit from modeling multiple funding and trust strategies before implementation.

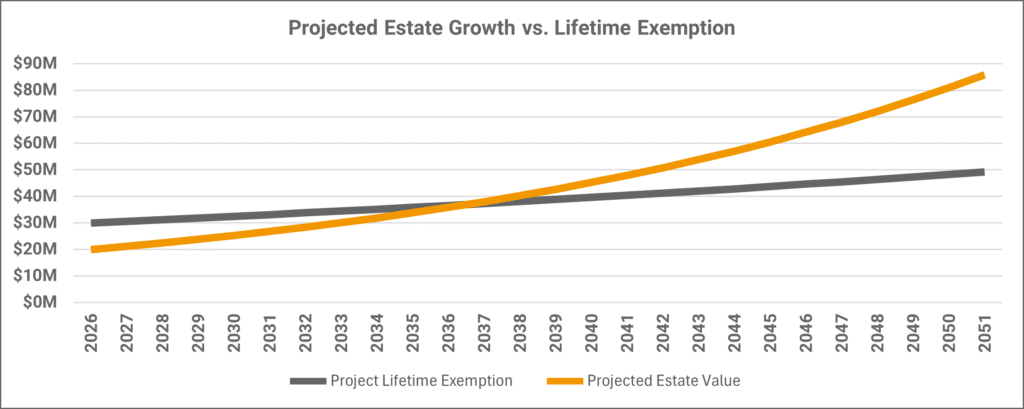

This chart assumes a $20 million estate growing at 5-percent annually compared to a $30 million lifetime exemption (married couple) indexed at 2-percent per year. Actual results will vary. For illustrative and discussion purposes only.

The objective is not simply to minimize tax. It is to protect the integrity of the estate plan across market cycles, legislative changes, and generational transitions.

The Lifetime Gift Tax Exemption as Part of a Larger Strategy

The 2026 lifetime gift tax exemption provides clarity. But clarity does not eliminate the need for disciplined planning.

Exemptions may change. Asset values fluctuate. Liquidity needs emerge unexpectedly.

Strategic lifetime gifting — when aligned with trust design and properly structured life insurance—can provide:

- Removal of future asset appreciation

- Estate liquidity without forced sales

- Greater intergenerational wealth control

- Long-term structural flexibility

Used thoughtfully, the exemption becomes part of a larger, coordinated estate strategy rather than a standalone tax maneuver.

Schedule a Confidential Estate Exemption Review

For families evaluating how the current lifetime gift tax exemption interacts with their estate, liquidity profile, and trust structures, a coordinated review can provide clarity.

At Mericle & Company, we work alongside estate planning attorneys, CPAs, and investment advisors to model:

- Current estate exposure

- Growth-based projections

- Liquidity requirements

- Trust and life insurance integration strategies

Our approach is data-driven and structure-focused. The goal is not simply to implement a transaction, but to ensure the design supports your family’s long-term objectives.

If you would like to review how the 2026 lifetime gift tax exemption fits within your broader estate plan, we welcome a confidential conversation.

Jason Mericle

Founder

Jason Mericle created Mericle & Company to provide families, business owners, and high net worth families access to unbiased life insurance information.

With more than two decades of experience, he has been involved with helping clients with everything from the placement of term life insurance to highly sophisticated and complex income and estate planning strategies utilizing life insurance.

Stay In The Know

Get exclusive tips and practical information to help you create, grow, sustain, and protect your wealth.

Ask Us Anything

We Are Here To Answer Your Questions

Start A Conversation

Schedule a complimentary 30 minute Zoom meeting to learn more about your options.