Premium Financing vs. Paying Cash for Life Insurance: How to Evaluate the Right Approach

For many high-net-worth individuals and families, the decision to acquire life insurance is relatively straightforward. The more nuanced question is how to fund it.

Should premiums be paid using available cash? Or should a financing strategy be considered?

Both approaches are widely used. Both can be appropriate. And both involve tradeoffs that extend beyond the policy itself — particularly when the goal is creating long-term estate liquidity.

Rather than focusing on which strategy is “better,” the better approach is to understand how each option interacts with assets of your estate and your long-term planning objectives. If you are evaluating this in the context of long-term planning, it may be helpful to revisit how estate liquidity planning fits into the overall picture.

What Does “Paying Cash” Involve?

Paying premiums in cash typically means using:

- Current income or excess cash flow

- Liquid assets

- Proceeds from repositioned investments

This approach is straightforward. It avoids borrowing, interest costs, and lender involvement.

At the same time, it requires a conscious decision about where capital is deployed. Funds used for premiums are no longer available for other purposes — whether that is investments, real estate, privately held stock, etc.

For some individuals, that tradeoff is entirely acceptable. For others, it may require closer evaluation.

What Is Premium Financing?

In contrast, premium financing involves borrowing funds (typically from a third-party lender) to pay life insurance premiums.

The borrower (often a trust) provides collateral and is responsible for loan interest, which may be structured in different ways depending on the arrangement.

The primary distinction is that capital that might otherwise be used to pay premiums remains deployed elsewhere.

For a more detailed breakdown, see our guide on what is premium financing life insurance.

This approach introduces its own set of considerations, including loan structure, interest rates, and ongoing management.

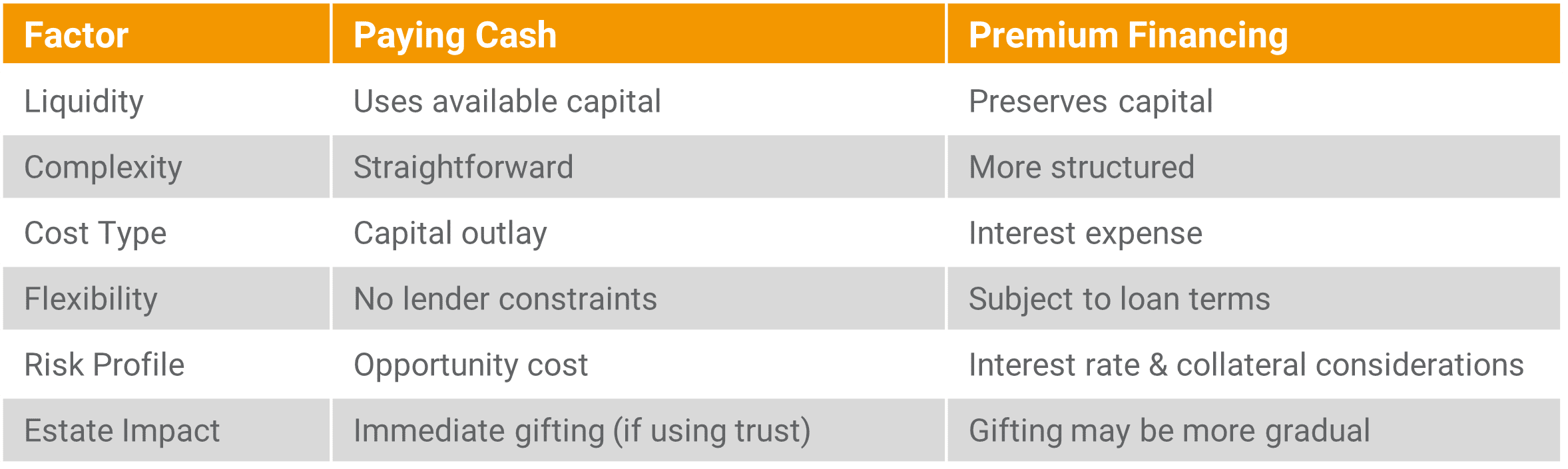

A Framework for Comparison

Instead of thinking about this as an either-or decision, it helps to understand both approaches from a few different perspectives.

- Liquidity and Capital Use

- Paying Cash: Reduces liquid assets or requires reallocating capital

- Premium Financing: Preserves liquidity but introduces a liability

The key question becomes: how important is it to maintain access to capital?

- Simplicity vs. Complexity

- Paying Cash: Operationally simple, with fewer moving parts

- Premium Financing: Requires coordination with lenders and ongoing monitoring

Some clients prioritize simplicity. Others are comfortable with added complexity if it aligns with broader objectives.

- Cost Structure

- Paying Cash: No borrowing costs, but involves the use of capital

- Premium Financing: Introduces interest expense and potential variability

Evaluating cost is not always straightforward, as it may depend on external factors such as interest rates and market conditions.

- Flexibility Over Time

- Paying Cash: Fewer external constraints once premiums are paid

- Premium Financing: May offer structuring flexibility but requires adherence to loan terms

Flexibility can be defined differently depending on the individual, either as independence from lenders or the ability to preserve capital for other uses.

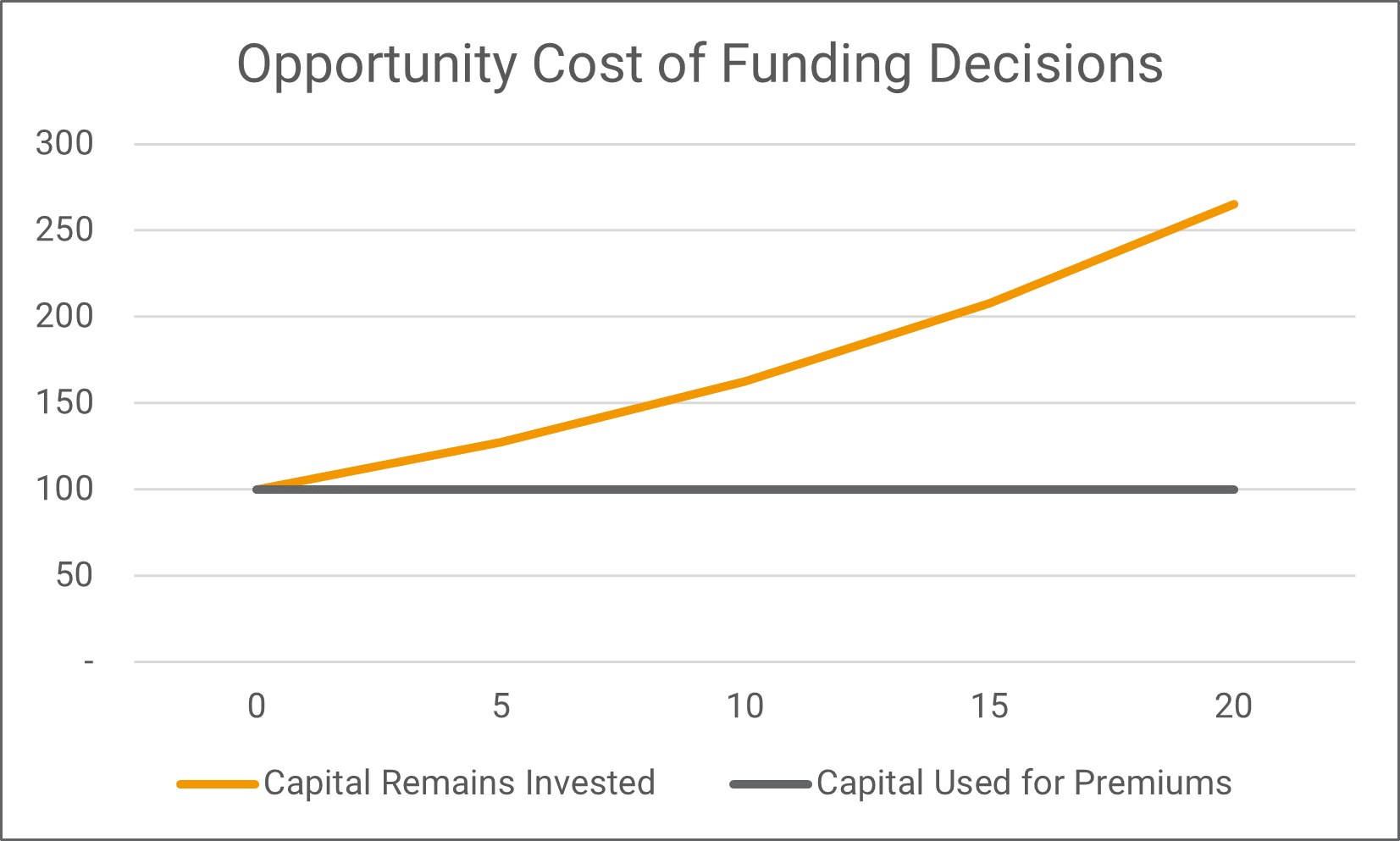

The Role of Opportunity Cost

Another important consideration is the concept of opportunity cost.

When capital is used to pay premiums, it is no longer available for other potential uses. When capital is preserved and premiums are financed, borrowing costs are introduced instead.

The relative impact of each depends on a range of variables, including:

- Expected investment returns

- Cost of borrowing

- Time horizon

- Risk tolerance

Because these variables differ from one client to another, the analysis is often specific to the individual situation rather than universally applicable.

This illustration is for conceptual purposes only. Actual outcomes depend on investment performance, borrowing costs, and individual circumstances.

How Gifting Strategies Can Influence the Decision

For individuals using life insurance within an irrevocable trust, the funding decision often ties directly to gifting.

When premiums are paid in cash, funds are typically gifted to the trust each year. These gifts may use the annual exclusion or a portion of the lifetime gift tax exemption. Over time, this can move a meaningful amount of assets out of the estate.

With premium financing, the structure may look different. In some cases, gifts are used to cover interest rather than the full premium. This can change the timing and amount of assets transferred.

For more on how these structures are typically designed, see our overview of an irrevocable life insurance trust.

As a result, each approach affects:

- How assets move out of the estate

- How gift tax exemptions are used

- How liquidity is managed at both the individual and trust level

For this reason, it is often helpful to evaluate funding strategies alongside a broader gifting plan, rather than in isolation.

Situations Where Paying Cash May Be Preferred

Paying premiums directly may be appropriate when:

- There is ample liquidity relative to the premium commitment

- Simplicity and control are primary considerations

- There is a limited desire to introduce leverage or external obligations

Situations Where Premium Financing May Be Considered

Premium financing may be worth evaluating when:

- Preserving liquidity is a priority

- Assets are concentrated or less liquid

- There is a desire to maintain existing investment allocations

For those exploring how this works in practice, reviewing a premium financing case study can provide additional context.

It’s Not Always an Either-Or Decision

In practice, funding strategies are not always static.

Some individuals choose to:

- Combine elements of both approaches

- Adjust funding methods over time

- Reevaluate the structure as market conditions or personal circumstances change

This flexibility can be an important part of the planning process.

Risk Considerations

Each approach carries its own risks.

Paying Cash:

- Reduced liquidity

- Potential need to liquidate assets at inopportune times

Premium Financing:

- Interest rate variability

- Collateral requirements

- Loan renewal considerations

Understanding and managing these risks is an essential part of the evaluation.

The Bottom Line: Alignment Matters More Than the Method

There is no universal answer to whether paying cash or using premium financing is the “right” approach.

The more relevant question is:

Which strategy aligns most closely with your overall financial structure, preferences, and long-term objectives?

For some, that will be simplicity and certainty. For others, it may be preserving capital and maintaining flexibility.

If you are evaluating how to fund a life insurance strategy, a side-by-side analysis can help clarify the tradeoffs in your specific situation.

We work with clients and their advisors to model different funding approaches so that decisions are grounded in a clear understanding of how each option may impact their broader financial picture.

If helpful, you can also review a premium financing case study to see how these strategies are structured in real-world scenarios.

Jason Mericle

Founder

Jason Mericle created Mericle & Company to provide families, business owners, and high net worth families access to unbiased life insurance information.

With more than two decades of experience, he has been involved with helping clients with everything from the placement of term life insurance to highly sophisticated and complex income and estate planning strategies utilizing life insurance.

Stay In The Know

Get exclusive tips and practical information to help you create, grow, sustain, and protect your wealth.

Ask Us Anything

We Are Here To Answer Your Questions

Start A Conversation

Schedule a complimentary 30 minute Zoom meeting to learn more about your options.